South Africa needs to start building EVs locally to keep up with the rest of the world, or risk being left behind when the UK and EU ban the import of Internal Combustion Engine (ICE) vehicles, the country’s largest export markets.

The bans will come into effect in 2030 (UK) and 2035 (EU), but exports have already contracted by nearly half from R837 million in 2021 to R421 million in 2022, according to Neale Hill, head of both the National Association of Automobile Manufacturers of South Africa (Naamsa) and Ford Africa.

Hiten Parmar, executive director at Electric Mission, says that if South Africa does not align itself to the global market, it could see reduced demand for vehicles manufactured locally. This will result in lower foreign direct investment, lower economic growth and lower job creation.

Parmer says that despite loadshedding, many businesses, malls, and public charging sites have back-up power for EV charging. “It has also become a stronger business case now for investments in solar, battery systems, EV charging infrastructure and fleets of EVs for corporate operations,” he says.

In addition to an electric powertrain, EVs have less than 20 moving parts versus around 2 000 on an ICE vehicle, making it significantly cheaper to maintain.

Strong case for EVs

BMW’s iX3 starts at R1 306 400, compared to R1 296 393 on its ICE counterpart, the X3 30d; it’s a R10 000 difference. A full charge on the 80kWh battery costs R470 at its maximum cost on a DC charger (R5.88 per kWh) compared to a 68L full tank on the X3 coming in at just under R1 400.

Given the price parity, the reduced number of parts for maintenance and lower cost of charging compared to fuel, it seems there’s a strong case to build EVs in South Africa for the local and export markets.

Parmar says the assembly of ICEs and EVs have common tooling and infrastructure, and so a model with both variants can be assembled on the same production line because the majority of the vehicle’s components are the same. There are, however, differences between the powertrain for ICEs and EVs.

“Engine manufacturing for ICE vehicles is currently done separately within the manufacturing environment, so will the electric motor system and battery packs for EV models. During the vehicle’s final assembly process, at the stage of powertrain installation, the specific engine or electric motor system is just installed, and the rest of the vehicle assembly continues through its normal process,” Parmar says.

Due to the high price of new EVs, there is now a very active market for secondhand vehicles, which still hold their residual value when sold as pre-owned, says Parmar. He adds that there’s a skills gap in repairing EVs. “It’s a specialised skill to be competent to work on high-voltage systems within electric vehicles.”

When it comes to battery components, Parmar says Sub-Saharan Africa has the minerals for EV production and with a consolidated regional effort, SADC countries could become important players in battery manufacturing, not only for EVs, but also for the energy industry.

“South Africa already has an active battery assembly market; however, based on the regional mineral wealth, this urgently needs to transform into battery manufacturing,” he says. “As supply-chain mechanisms change, with more emphasis on sustainability, it’s imperative that battery manufacturing takes place in South Africa.”

Winstone Jordaan, director at GridCars, says that the longer the country takes to start investing in the transition, the fewer opportunities will be available, and the more it will need to invest to speed up the change in a more competitive market.

“Other countries across the world, including African countries, spend their time and effort exploring opportunities in the industry, such as developing IP and investing in designs,” says Jordaan.

Parmar adds that incentives for EVs and EV component production will be important in transforming the local industry. “The growth of automotive manufacturing from 1924 to date has been on the back of government’s manufacturing incentives, but there are no specific incentives for EV manufacturing over ICEs.”

Jordaan says he can’t understand what’s holding the government back, other than an “obsession with the coal value chain, and an underestimation of the value that EVs will bring to the market.

“We still have people playing it safe within the New Energy Vehicle (NEV) space by keeping room for other alternatives. This is causing some hesitation to fully commit to a predominantly EV strategy,” he says.

He believes when the NEV policy is implemented, many of the plans will be outdated because it was based on 2020 data when three million EVs were sold globally. “Since then, seven million EVs were sold in 2021, and over 10 million in 2022. In two years, while the paper has been ‘in process’, the world’s EV fleet has almost tripled.”

As developing nations, Parmar thinks South Africa and India are comparable. “India has a well-established automotive manufacturing industry, with EV production already active; some of the key differentiators are that the Indian government declared a ban of ICE vehicles by 2030, and also has multiple incentives for the EV value chain. Currently, South Africa is lagging far behind India in the overall context across EVs.”

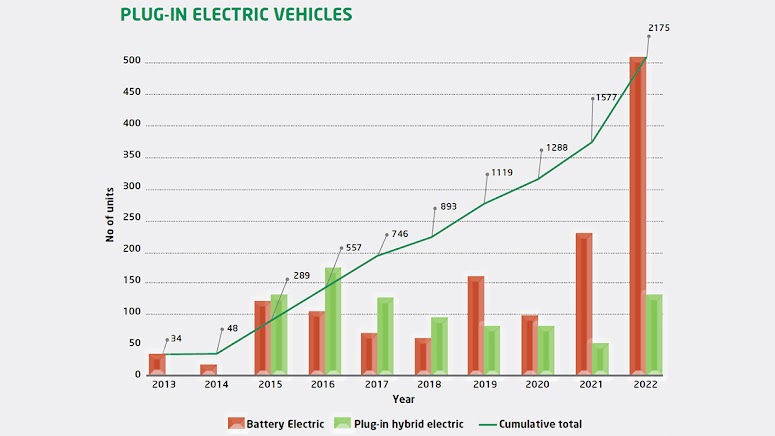

Parmar says he’s seeing increased demand for EVs in South Africa. In 2019, there was a technology shift from plug-in hybrids to full battery EVs, which illustrates that South African consumers now have more confidence in EVs, he says.

“Locally produced EVs, specifically EV components, should effectively reduce the retail price of EVs,” says Parmar. “Manufacturers would drive local investment into EVs, with production incentives being made available as there are many other countries competing with South Africa for automotive production. It can only benefit South Africa holistically.”

Originally published here: https://brainstorm.itweb.co.za/content/dgp45MaBx21qX9l8

Recharged is an independent site that focuses on technology, electric vehicles, and the digital life by Nafisa Akabor. Drawing from her 19-year tech journalism career, expect news, reviews, how-tos, comparisons, and practical uses of tech that are easy to digest. Nafisa is a traveller at heart, having been to 46 countries and counting. Find her edutainment videos covering tech, EVs and travel on TikTok.